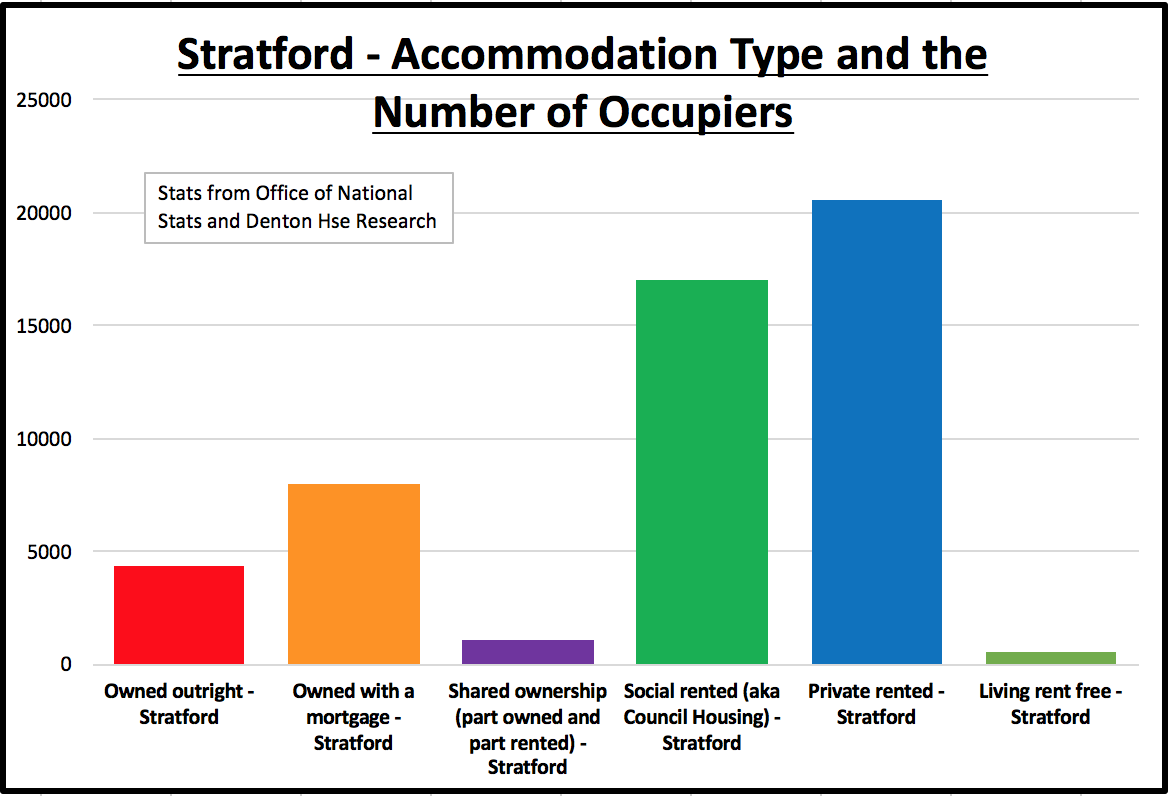

“The mortgage market is in continuous move and it can affect you as well. ”

If you’re one of those shopping for a house soon and you are considering a mortgage, you should carefully analyse a couple of factors before making a decision. The location, the time you are going to spend in your new home (if it is temporary or, hopefully, for the rest of your life), the purpose of the investment (for your own living or if it is a buy to let), and other life circumstances should be considered when choosing a type of mortgage.

If you’re one of those shopping for a house soon and you are considering a mortgage, you should carefully analyse a couple of factors before making a decision. The location, the time you are going to spend in your new home (if it is temporary or, hopefully, for the rest of your life), the purpose of the investment (for your own living or if it is a buy to let), and other life circumstances should be considered when choosing a type of mortgage.

However, even with all these cleared up, there is still one more factor that might influence your decision. The mortgage market is in continuous move and it can affect you as well.

The analysis after the first quarter of 2017 proves that some types of mortgages are increasing, while other products for loans are remaining unchanged. For example, the number of contracted mortgages rose in the first three months. These are bank products offered for self-employed people, people with complex incomes or other underserved segments of the buyers’ market. Looking closely upon the offer of bank products, you may see that banks will speculate this moment and will come with new and improved offers. You will just have to pick the most advantageous for you.

The mortgage market also seems to be improving since the number of completed applications for first time buyers is rising. 67% of first time mortgage applications were completed in the first quarter of 2017, up substantially from 48% in the same period of 2016. Intermediaries have eased up the applications because of the struggle to obtain a mortgage that was intensely publicised last year.

The mortgage market also seems to be improving since the number of completed applications for first time buyers is rising. 67% of first time mortgage applications were completed in the first quarter of 2017, up substantially from 48% in the same period of 2016. Intermediaries have eased up the applications because of the struggle to obtain a mortgage that was intensely publicised last year.

And one of the most important news that the mortgage market received at the beginning of this month is that the lending rates reached their lowest point. The figures from the Bank of England showed that this year’s borrowers received the lowest mortgage rates ever.

These effects are sometimes connected and influence one another, but paying enough attention to the movements of the market might pay off eventually.

Sources:

http://www.propertywire.com/news/uk/brokers-see-demand-specialist-mortgages-less-buy-let-forecast/

http://www.propertywire.com/news/uk/uk-mortgage-applications-intermediaries-successful-year-ago/

http://www.propertywire.com/news/uk/mortgage-lending-rates-uk-reaching-lowest-rates-ever/

Buying a home for the first time is one of the biggest decisions you will make.

Buying a home for the first time is one of the biggest decisions you will make.